You open your renewal notice and your homeowners insurance premium jumped again.

Then you hear people saying roof claims are changing, older roofs may be treated differently, deductibles are getting tougher, and insurance companies are looking more closely at storm damage.

Here’s what that usually means.

North Carolina homeowners are entering a more expensive, more selective insurance market in 2026. That does not mean every roof claim will be denied. It does not mean insurance will automatically replace your roof after a storm. It means homeowners need to understand their policy before the next storm, not after water is already coming through the ceiling.

Quick Answer

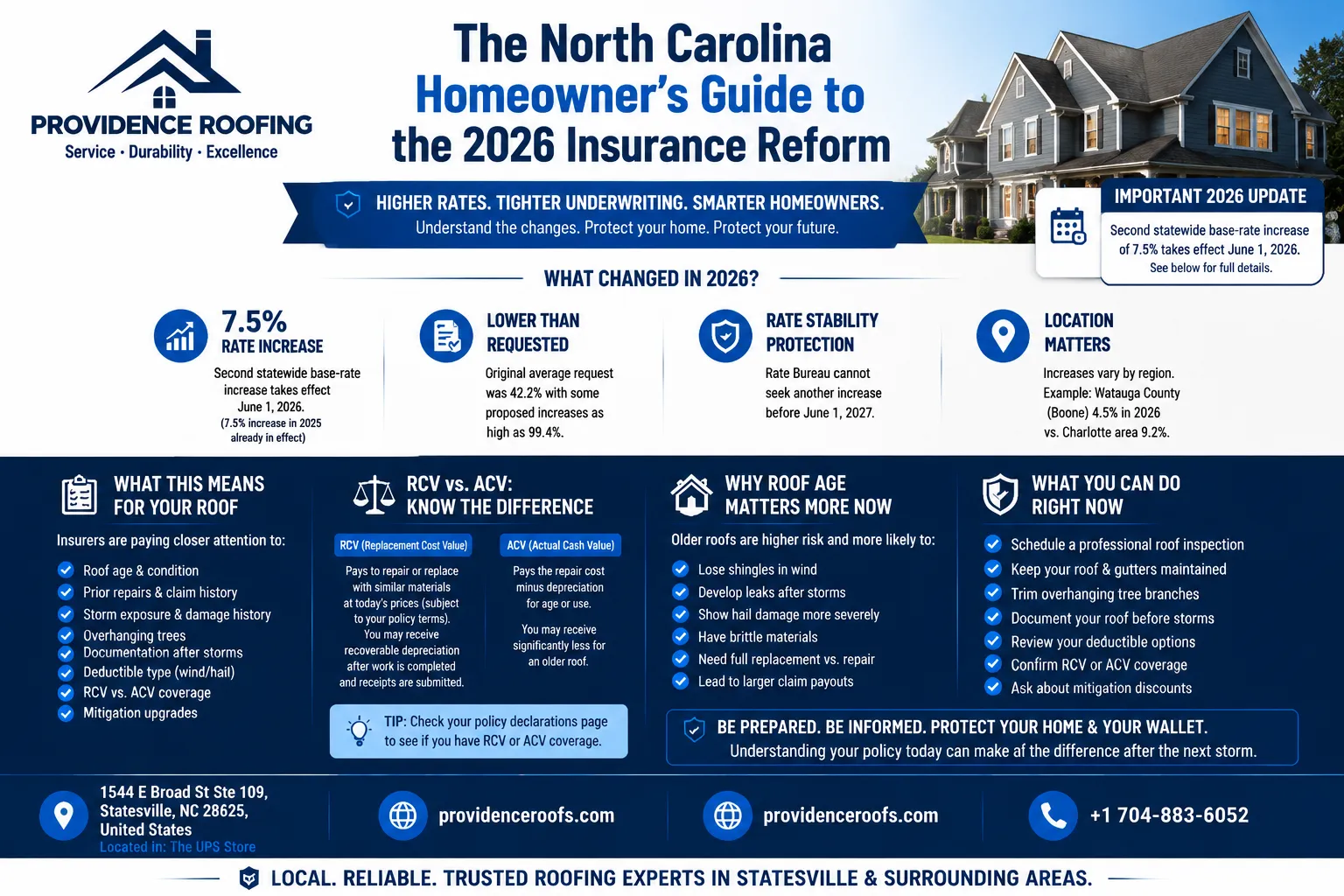

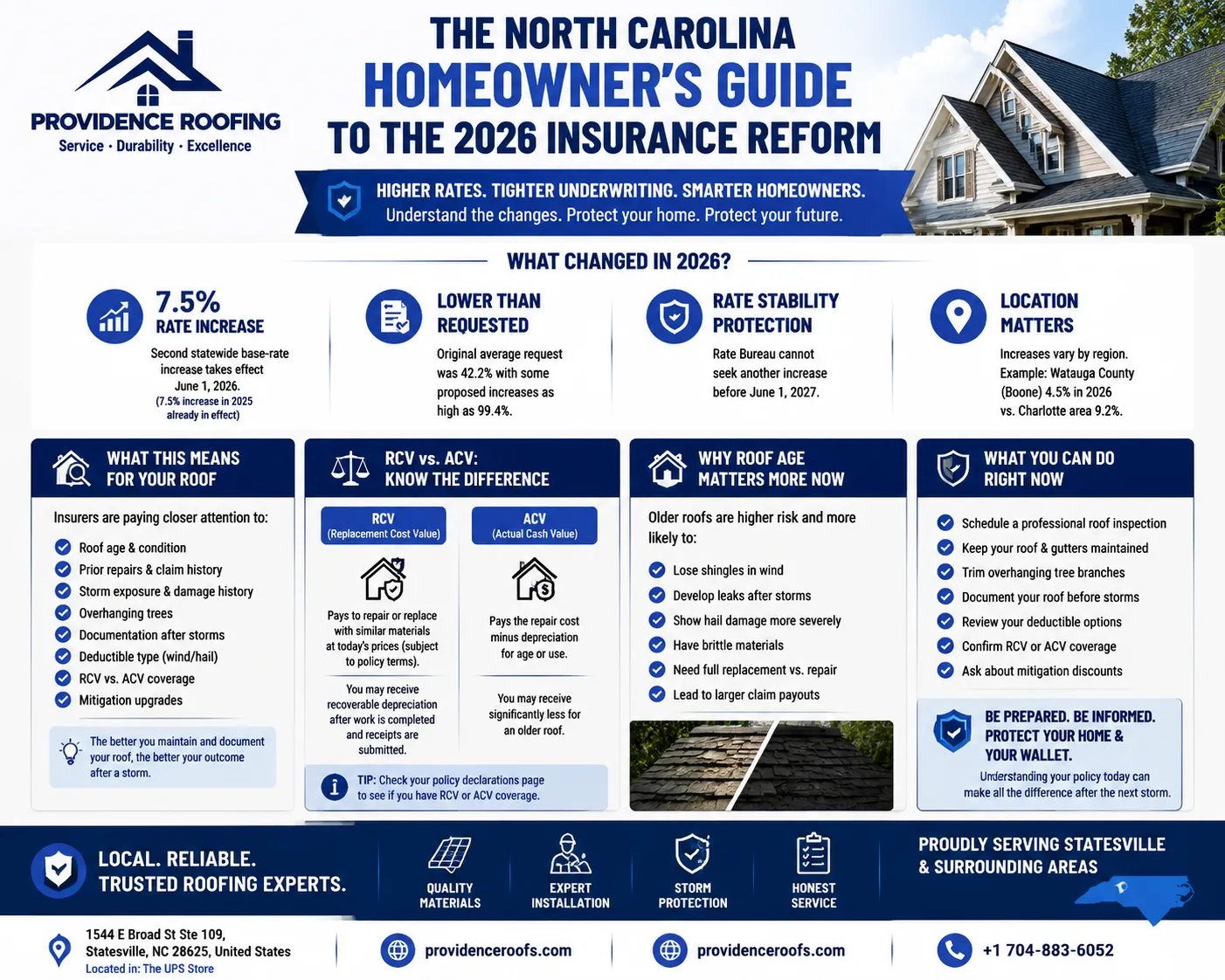

North Carolina’s major 2026 homeowners insurance change is a second statewide base-rate increase of 7.5% taking effect June 1, 2026, following a 7.5% increase in 2025. The settlement came after the North Carolina Rate Bureau originally requested an average 42.2% increase, with some proposed increases as high as 99.4% in certain areas. The settlement also prevents the Rate Bureau from seeking another increase before June 1, 2027.

For roof owners, the bigger practical shift is this:

Insurance companies are paying closer attention to roof age, roof condition, claim history, storm exposure, and whether your policy pays Replacement Cost Value or Actual Cash Value.

That is the part that can affect how much money you actually receive after wind, hail, or storm damage.

What Changed in 2026?

The headline change is the rate increase.

The North Carolina Department of Insurance announced that the statewide homeowners insurance base rate would increase by 7.5% on June 1, 2025, and another 7.5% on June 1, 2026. That is far lower than the industry’s original 42.2% average request, but it still means many homeowners will feel higher premiums.

The increase is not identical everywhere. AP reported that location matters: Charlotte-area base rates were set to rise 9.3% in 2025 and 9.2% in 2026, while Watauga County, which includes Boone, was set for lower increases of 4.4% in 2025 and 4.5% in 2026.

That matters for Providence Roofing homeowners across North Carolina because the pressure is not the same in every market.

A roof in Carolina Shores faces different insurance concerns than a roof in Boone. A roof in Huntersville may be rated differently than a roof in Hickory or Morganton. Storm exposure, claims history, coastal risk, mountain weather, and local construction costs all matter.

What This Means for Your Roof

Insurance companies are trying to price risk more tightly.

Roofs are one of the biggest risk items on a homeowners policy because wind, hail, falling limbs, hurricanes, and heavy rain often show up first on the roof. When roofing labor and material prices rise, roof claims become more expensive too.

So in 2026, homeowners should expect more attention on:

- Roof age

- Roof condition

- Prior repairs

- Missing or damaged shingles

- Granule loss

- Hail or wind history

- Overhanging trees

- Documentation after storms

- Deductible type

- Whether the roof is insured at RCV or ACV

- Whether mitigation upgrades may help

This does not mean you should panic-replace a roof that still has life left.

You may not need a full replacement.

But you do need to know what your insurance company sees when they look at your roof.

The Most Important Terms: RCV vs. ACV

This is where homeowners get surprised.

Replacement Cost Value

Replacement Cost Value, or RCV, generally means the amount needed to repair or replace damaged property at today’s prices, subject to policy terms, deductible, and coverage limits. The North Carolina Department of Insurance explains that replacement cost reflects today’s cost of building supplies or replacing property with a similar item.

With many RCV claims, the insurance company may first pay the Actual Cash Value amount. Then, after the work is completed and receipts are submitted, the carrier may reimburse the recoverable depreciation. NCDOI describes this second payment as “recoverable depreciation.”

Actual Cash Value

Actual Cash Value, or ACV, means the repair cost minus depreciation for age or use. NCDOI also calls this depreciated cash value.

Here is the plain-English version:

If your older roof is covered at ACV, you may receive much less than the cost of a new roof after a covered claim because depreciation is deducted.

That difference can be thousands of dollars.

Example: Why ACV Can Shock Homeowners

Let’s say a storm damages an older asphalt shingle roof.

A replacement might cost $16,000.

Your deductible is $2,500.

If the policy pays RCV, you may eventually receive more of the replacement cost, depending on policy terms and required documentation.

If the policy pays ACV, depreciation may be subtracted first. On an older roof, that could leave the homeowner responsible for a much larger share of the project.

That is why the most important insurance question is not:

“Do I have homeowners insurance?”

The better question is:

“How does my policy pay for roof damage?”

Why Roof Age Matters More Now

Older roofs are becoming a bigger underwriting issue.

That does not mean every older roof is bad. Some older roofs are well-maintained, properly ventilated, and still performing. Others are brittle, losing granules, lifting at the edges, or patched in multiple places.

Insurance companies care because older roofs are more likely to:

- Lose shingles during wind

- Develop leaks after storms

- Show hail damage more severely

- Have brittle shingles

- Need full replacement instead of repair

- Create larger claim payouts

- Hide decking or ventilation problems

A 17-year-old roof in Boone with ice-dam history is not the same risk as a 7-year-old roof in Statesville. A coastal Carolina Shores roof with wind exposure is different from a shaded Hickory roof under heavy tree cover.

The right answer depends on the actual roof.

Does Insurance Still Cover Storm Damage?

Yes, when the damage is covered by the policy and approved by the carrier.

But do not assume every roof problem is an insurance claim.

Insurance may apply when damage is sudden and storm-related, such as:

- Wind damage

- Hail damage

- Falling tree limbs

- Certain storm-related roof openings

- Covered water intrusion from a storm-created opening

Insurance usually does not cover:

- Normal aging

- Wear and tear

- Old shingles reaching the end of life

- Poor maintenance

- Improper installation

- Long-term leaks

- Rot that developed over time

- Cosmetic issues excluded by the policy

- Flood damage under a standard homeowners policy

Coverage depends on your policy, deductible, cause of damage, inspection findings, and carrier approval.

A roofer can document visible roof damage. A roofer cannot promise your claim will be approved.

What to Do Before Filing a Roof Claim

Do not file blindly.

A claim may make sense if there is clear storm damage, but filing without understanding the roof condition and deductible can create frustration.

Before filing, take these steps:

- Check your policy type.

Look for RCV, ACV, wind/hail deductible, named storm deductible, exclusions, and roof age limitations. - Document the storm.

Take photos of missing shingles, dents, leaks, fallen limbs, damaged gutters, or interior stains. - Get a roof inspection.

Ask for photos and a plain explanation of whether the damage looks storm-related, age-related, or installation-related. - Compare the damage to your deductible.

If the damage is minor and below the deductible, a claim may not help. - Talk to your insurance carrier or agent.

Ask how the policy would respond before assuming coverage.

The safest next step is information, not panic.

How This Affects Different North Carolina Homeowners

Boone and the High Country

Boone homeowners deal with snow, ice, freeze-thaw cycles, steep roofs, wind, and storm exposure. Ice dam leaks, winter damage, and ventilation problems may not always be treated like sudden storm damage. Documentation matters.

Hickory and Morganton

Foothills homes often deal with wind-driven rain, older roofs, shaded lots, and tree coverage. Granule loss, flashing issues, and limb damage should be documented carefully after storms.

Huntersville and Statesville

These fast-growing suburban areas often have larger rooflines and storm exposure. Hail and wind can create hidden damage that is not obvious from the ground.

Winston-Salem and the Triad

The Triad has mixed older and newer housing stock. Insurance questions often come down to roof age, prior repairs, and whether storm damage is isolated or widespread.

Carolina Shores

Coastal-adjacent roofs face stronger wind, humidity, salt air, and storm-system risk. Homeowners should pay especially close attention to wind/hail deductibles, named storm provisions, and mitigation options.

Fortified Roofs and Why They Matter

North Carolina has been pushing stronger roofing systems, especially in coastal areas.

The North Carolina Department of Insurance says the state ranks second in the nation in fortified roofs and highlighted NCIUA grant programs that help homeowners install IBHS FORTIFIED Roofs. NCDOI also cited an N.C. State University study showing fortified-roof homes were 34% less likely to file a claim after several hurricanes, and when claims were filed, damage was 22% less severe than standard-roof homes.

That does not mean every homeowner can get a grant. It does not mean every roof needs a fortified upgrade. But it shows where the insurance market is heading:

Stronger roofs are becoming part of the insurance conversation.

For coastal and storm-exposed homes, the roof system may matter as much as the shingle brand.

Questions to Ask Your Insurance Agent in 2026

Before the next storm, ask your agent these questions:

- Is my roof covered at Replacement Cost Value or Actual Cash Value?

- Does my roof coverage change after a certain roof age?

- Do I have a separate wind or hail deductible?

- Do I have a named storm deductible?

- Are cosmetic hail impacts excluded?

- Are matching shingles covered if only one slope is damaged?

- What documentation do I need after a storm?

- Does my policy include code upgrade coverage?

- Are there discounts for fortified roofing or mitigation upgrades?

- Could my roof condition affect renewal?

Do not wait until an adjuster is standing in your yard to learn the answer.

Questions to Ask a Roofer Before an Insurance Claim

A good roofer should be able to show you what they see.

Ask:

- Is the damage storm-related or age-related?

- Is the roof repairable?

- Are there missing shingles, lifted shingles, or hail bruises?

- Is the decking soft or damaged?

- Are there photos of each problem area?

- Are the gutters, vents, flashing, and ridge caps damaged too?

- Is there interior or attic evidence of water intrusion?

- Would this likely be above or below my deductible?

- Do I need emergency repair to prevent more damage?

The roofer should not pressure you into a claim. The roofer should help you understand the roof.

The Big Mistake Homeowners Make

The big mistake is assuming insurance will “take care of it.”

That used to be a common mindset.

In 2026, it is risky.

A homeowner may discover:

- The deductible is higher than expected

- The roof is paid at ACV

- The damage is considered wear and tear

- The roof is too old for full replacement cost

- The claim only covers a repair

- Matching is not covered the way they assumed

- Interior damage is handled differently than roof damage

- The policy has exclusions they did not know about

That does not mean insurance is useless. It means the policy language matters.

Should You Replace Your Roof Before Insurance Forces the Issue?

Maybe, but not automatically.

You may not need a full replacement if:

- The roof is still performing

- Shingles are sealed and not brittle

- Damage is isolated

- Decking is solid

- Flashing is in good shape

- Ventilation is working

- Repairs are reasonable

Replacement may make more sense if:

- The roof is near the end of its life

- You have repeated leaks

- Shingles are curling, cracking, or missing

- Granule loss is heavy

- Storm damage is widespread

- Decking is soft

- Insurance renewal is becoming a concern

- You plan to sell and the roof will become a negotiation issue

Don’t guess from the ground.

A roof inspection can help you decide whether you need repair, maintenance, documentation, or replacement.

Bottom Line

The 2026 North Carolina insurance reform does not mean every homeowner suddenly needs a new roof.

It means homeowners need to understand the financial side of roof damage before the next storm.

The key changes and trends are:

- Homeowners insurance base rates are increasing again on June 1, 2026.

- Roof age and condition are getting more attention.

- RCV vs. ACV can dramatically change claim payouts.

- Wind, hail, and named-storm deductibles matter.

- Fortified and stronger roof systems are becoming more important in storm-prone areas.

- Insurance may cover storm damage, but it does not cover normal aging or every roof problem.

If you are not sure whether your roof is ready for the next storm, Providence Roofing can inspect it, document what we see, and help you understand whether you need a repair, replacement, or just a clearer conversation with your insurance agent.